Navigating small business health insurance in Maryland can feel overwhelming, especially for companies with less than 20 employees.

This guide aims to give employers insight and simplify the process of offering health benefits to your team.

We’ll break down essential aspects of small business health insurance in Maryland, including:

- Requirements for small business

- Fully-insured vs level-funded plans

- Cost of small business health insurance

- Working with a health insurance broker

Finding the right health insurance for your Maryland small business is crucial for attracting and retaining top talent, boosting employee morale, and ensuring the overall well-being of your team.

Let’s explore how to find the best health insurance for your business and your team!

Free Assistance

As an independent health insurance broker, we specialize in helping small businesses in Maryland with top-rated plans and benefits from carriers like: Aetna, UnitedHealthcare, MetLife and more.

We make it easy online with enrollment, employee consultations, and renewals with free personalized guidance from a licensed expert from start to finish.

Ready to get started? Call, chat or schedule a consultation today!

Maryland Small Business Health Insurance Requirements

The IRS and SBA have different criteria to define a small business, but when it comes to small business health insurance requirements it’s the Affordable Care Act (ACA) definition.

According to ACA, if you’re in business with less than 50 full-time employees you are not required to provide health insurance to your workers.

Companies with more than 50 are required to offer health insurance.

If you’re here you probably know offering health insurance has many advantages:

- Affordable health, dental & vision benefits

- Potential tax savings and deductions

- Happy and more productive work environment

What is the Minimum Number of Employees?

Before you dive into small business health insurance in Maryland you’ll have to determine your eligibility:

- A principal business address in Maryland

- Federal employer identification number (EIN)

- Less than 50 full-time equivalent employees (FTEs)

Most major insurance carriers will require two full-time employees to establish a small group.

Some top-rated carriers like Aetna and UnitedHealthcare have large provider networks in Maryland with flexible plan designs.

Small Business Health Insurance Options in Maryland

When shopping for small business health insurance in Maryland, there are two main options: on-exchange and off-exchange plans.

The Small Business Health Options Program or SHOP, is accessible through the Maryland Health Connection and tailored to small employers.

What is Maryland Health Connection for Small Business?

Maryland Health Connection (MHC) is the state’s health insurance marketplace for individual plans.

Marketplace plans are also referred to as “on-exchange” plans.

The business portal was specifically designed to streamline the process of obtaining Maryland small business health insurance for companies with less than 50 full-time employees.

Business owners can start a quote and get free assistance from licensed insurance brokers that have partnered with Maryland Health Connection.

You do not have to go through Maryland Health Connection for small group health insurance unless you want to claim the Small Business Health Care Tax Credit.

Be sure to consult with your tax advisor with any questions about the credit.

A broker can help you choose the right plans, educate your employees, help navigate the enrollment process, and provide expert advice on selecting the best options for your team.

- Key Features:

- Year-Round Enrollment: Unlike individual marketplaces, SHOP allows for enrollment throughout the year.

- Employer Flexibility: Employers can customize their contribution levels toward employee premiums.

- Potential Tax Credits: Eligible businesses may qualify for the Small Business Health Care Tax Credit, reducing premium costs.

- ACA Compliance: SHOP plans adhere to the Affordable Care Act (ACA), ensuring guaranteed issue and community rating, which prohibits pre-existing condition exclusions and provides predictable coverage.

- Fully Insured: SHOP plans are fully-insured. (see below)

Off-Exchange Group Plans

Off-exchange plans are purchased directly from insurance companies and brokers outside of the marketplace. These plans can offer:

- Greater Flexibility: Off-exchange plans often provide greater flexibility in plan design, pricing (see level-funded plans below), and provider network.

- Streamlined Enrollment: The enrollment process for off-exchange plans can be more streamlined, with some carriers offering digital enrollment platforms. SHOP plans typically require additional paperwork.

- Level-Funded Options: Shopping off-exchange opens the door to more options. Level-funded plans are typically less expensive than traditional fully-insured options. (see below)

Off-exchange plans have some important considerations:

Medical Questionnaires and Underwriting: To obtain the best rates, insurance companies may require medical questionnaires or other underwriting processes.

This can be a barrier for some businesses or lead to higher premiums if members of the group have known pre-existing conditions.

No Small Business Tax Credit: Businesses purchasing off-exchange plans are not eligible for the Small Business Health Care Tax Credit.

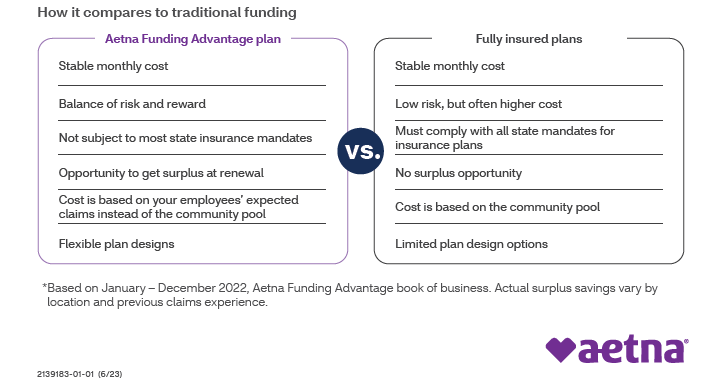

Comparing Fully-Insured vs. Level-Funded

As a small business owner in Maryland, you’re likely familiar with the rising costs of employee healthcare.

There are two primary funding models for small business health insurance: fully-insured and level-funded.

- Fully-insured Plans: Shift the risk of high medical claims to the insurance carrier.

- Level-funded Plans: Share some risk with the employer, but mitigated by a claim reserve and stop-loss insurance.

Fully-insured health plans are the traditional, most familiar route for most Maryland small businesses.

Your group is community rated, meaning employees in good health are grouped with employees that are not so healthy to determine what you pay.

Fully-insured plans are also the most expensive option.

Your company pays a fixed monthly premium to the insurance carrier, which assumes the entirety of the financial risk associated with employee medical claims.

Pros

- Predictable Costs: Premiums are fixed, making budgeting straightforward

- Guaranteed Coverage: ACA compliant, no pre-existing condition exclusions

Cons

- Higher Premiums: Insurers take on all risk making these plans more expensive.

- Less Flexibility: Usually limited to in-network providers only.

- No Rebates: Surplus funds are not returned to the group.

Ideal for: Maryland small businesses prioritizing simplicity and stability over cost savings, particularly those with a diverse health risk profile among employees

Level-Funded Health Plans

Level-funded health plans are gaining traction as a cost-effective and flexible alternative to traditional fully-insured options.

These plans combine elements of self-insurance and conventional insurance.

Employers pay a fixed monthly amount that covers projected claims, administrative fees, and stop-loss insurance premiums.

Level-funded plans require underwriting based on employee medical history, typically the past five years.

In the event of lower-than-anticipated claims, employers may be eligible for a refund of surplus funds.

Pros

- Affordability: Cost based on your group, not community rates

- Plan Flexibility: Expanded offering with out-of-network coverage

- Limited Liability: Calculated claims reserve and stop-loss policy included

- Incentives & Rebates: Potentially based on end-of-year group claims history

Cons

- Health Questions: Employees will have to submit medical history for underwriting

- Plan Start Date: Effective dates are typically only the first of the month

Ideal for: Businesses with a relatively healthy employee population seeking greater flexibility and potential cost savings with return on investment.

Cost of Maryland Small Business Health Insurance

The cost of health insurance for your Maryland small business requires an assessment beyond just price.

While company size and plan type are important, employee demographics play a crucial role.

You’ll need to align affordability with the specific healthcare needs of your workforce.

Fully-Insured

In Maryland, the average annual premium per employee in 2023 was approximately $7,800, or $650 per month.

Based on this figure, a fully-insured group plan for 5 full-time employees might range $3,000-$3,500 per month.

Level-Funded

To illustrate the potential savings of a level-funded plan, look at this example for medical coverage with 5 employees.

Estimated monthly costs on selected plans range $2,000-$2,500, or $400-$500 per employee.

Contact us for a free custom quote tailored to your business’s specific needs and employee demographics.

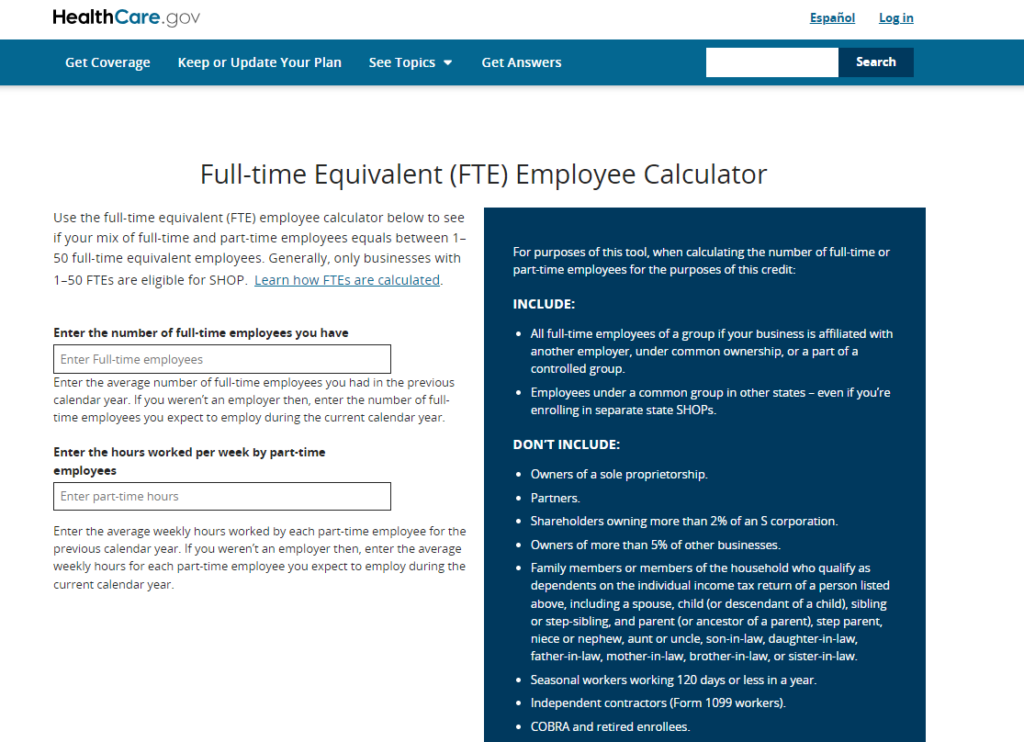

Calculating Full-Time Employees (FTE)

Ensuring that your employees are eligible for your small business’s health insurance benefits is an essential step.

Here’s how you can determine eligibility at Healthcare.gov using the FTE Calculator:

1. Define Full-Time Employees: In Maryland, a full-time employee is generally someone who works at least 30 hours per week. It’s essential to establish these criteria upfront to identify those employees who qualify for healthcare benefits.

2. Calculate Full-Time Equivalent Employees: If you have a combination of full-time and part-time employees, you’ll need to calculate full-time equivalent (FTE) employees. This calculation considers the total number of hours worked by part-time employees and adds them to the count of full-time employees.

If your business meets this requirement, you are eligible to offer health insurance coverage to your employees.

By following these steps and making use of Maryland Health Connection, you can streamline the process of securing healthcare benefits for your small business while ensuring that you meet the eligibility requirements for your employees.

This will enable you to provide valuable health coverage to your workforce, enhancing their well-being and the overall appeal of your business.

Free Consultation

Our team is dedicated to making it easy for individuals, families & small business owners to find affordable plans & benefits.

Start a quote or schedule a free consultation today!

Privacy is our priority. We don’t share your personal information or collect payments for your peace of mind.

That’s BenZen.

Ted McNeil

Owner, Broker

BenZen Insurance